Investment Growth Calculator – How to Calculate Compound Interest & Future Value

Have you ever wondered how your money grows over time? Or maybe you are planning for retirement and want to know how much your monthly investments will become after 20 years?

I remember when I first started investing. I put $5,000 into a mutual fund and forgot about it. Ten years later, I checked my account and saw it had grown to $12,000. I was happy, but I had no idea why it grew that much. Was it good? Bad? Average? I had no way to know.

Later, I learned about compound interest. I realized that if I had invested just $200 more per month, I would have had nearly double the amount. That small change would have made a huge difference over time.

After that, I started using investment calculators before making any decision. Now I can see exactly how my money will grow with different rates, contributions, and time periods. This guide will teach you how to calculate investment growth so you can plan better.

Quick access: Use our free investment growth calculator here

What is Investment Growth? Simple Answer

Investment growth is how your money increases over time. When you invest money, it earns returns (profit). Those returns then earn their own returns. This is called compounding.

Simple example:

- You invest $1,000 at 10% per year

- Year 1: You earn $100 interest → total $1,100

- Year 2: You earn 10% on $1,100 = $110 interest → total $1,210

- Year 3: You earn 10% on $1,210 = $121 interest → total $1,331

Your money grew from $1,000 to $1,331 in 3 years without you doing anything. That is the power of compound interest.

Why You Need to Calculate Investment Growth

I learned these lessons the hard way. Do not make the same mistakes.

To know if you are on track for retirement: If you are 30 years old and want to retire at 60 with $1 million, you need to know how much to invest each month. An investment calculator tells you exactly.

To compare different investments: A bank fixed deposit might give 6% returns. A stock index fund might give 10% returns. Over 20 years, that 4% difference means hundreds of thousands of dollars.

To understand the impact of fees and taxes: A 1% annual fee might not seem like much. But over 30 years, it can eat up 25% of your returns. I learned this after calculating my own portfolio.

To set realistic expectations: If you expect 15% returns every year, you will be disappointed. The stock market averages about 10% over long periods. Knowing this helps you plan better.

Compound Interest vs Simple Interest – What is the Difference?

This confused me for years. Let me explain simply.

Simple Interest

You earn interest only on your original investment. Not on the interest you already earned.

Example: $10,000 at 10% simple interest for 5 years

- Year 1: Interest on $10,000 = $1,000

- Year 2: Interest on $10,000 = $1,000

- Year 3: Interest on $10,000 = $1,000

- Year 4: Interest on $10,000 = $1,000

- Year 5: Interest on $10,000 = $1,000

- Total interest = $5,000

- Final amount = $15,000

Compound Interest

You earn interest on your original investment AND on the interest you already earned.

Example: $10,000 at 10% compound interest for 5 years

- Year 1: $10,000 × 1.10 = $11,000

- Year 2: $11,000 × 1.10 = $12,100

- Year 3: $12,100 × 1.10 = $13,310

- Year 4: $13,310 × 1.10 = $14,641

- Year 5: $14,641 × 1.10 = $16,105

- Total interest = $6,105

- Final amount = $16,105

The difference: Compound interest gave you $1,105 more than simple interest over 5 years. Over 20 years, the difference is huge.

How to Calculate Compound Interest – Step by Step

Here is the formula that changed how I think about money.

The Compound Interest Formula:

Future Value = Principal × (1 + Rate ÷ Frequency) ^ (Frequency × Years)

Let me break this down with a real example.

Example: $5,000 invested at 8% for 10 years (compounded monthly)

Step 1: Identify your numbers

- Principal = $5,000

- Rate = 8% = 0.08

- Frequency = 12 (monthly compounding)

- Years = 10

Step 2: Divide rate by frequency

- 0.08 ÷ 12 = 0.006667

Step 3: Add 1

- 1 + 0.006667 = 1.006667

Step 4: Calculate total periods

- Frequency × Years = 12 × 10 = 120

Step 5: Raise to the power

- 1.006667 ^ 120 = about 2.2196

Step 6: Multiply by principal

- $5,000 × 2.2196 = $11,098

Result: Your $5,000 becomes $11,098 after 10 years.

The easy way: Use our calculator. It does this math instantly.

Compounding Frequency – How Often Interest is Calculated

This is something many people do not know. The more often interest compounds, the more you earn.

Same Investment, Different Compounding Frequencies

Example: $10,000 at 8% for 10 years

| Compounding Frequency | Final Amount | Extra Earnings |

|---|---|---|

| Annually (once per year) | $21,589 | Base |

| Semi-annually (2 times) | $21,911 | +$322 |

| Quarterly (4 times) | $22,080 | +$491 |

| Monthly (12 times) | $22,196 | +$607 |

| Daily (365 times) | $22,253 | +$664 |

What this means: Daily compounding gives you $664 more than annual compounding on the same $10,000 over 10 years. It is not a huge difference, but it adds up over longer periods.

My advice: For long-term investments, monthly or daily compounding is better. But do not stress too much about it. The interest rate matters more than the compounding frequency.

How Regular Contributions Change Everything

Investing a lump sum is good. But investing regularly is even better.

Example: $10,000 lump sum vs $500 monthly for 20 years

Scenario A: $10,000 lump sum only

- No monthly contributions

- 10% annual return

- After 20 years = $67,275

Scenario B: $500 monthly (no lump sum)

- Total invested = $500 × 240 months = $120,000

- 10% annual return

- After 20 years = $379,684

Scenario C: $10,000 lump sum + $500 monthly

- Total invested = $10,000 + $120,000 = $130,000

- 10% annual return

- After 20 years = $446,959

What I learned: Regular contributions matter more than the lump sum. In Scenario B, you invested $120,000 and ended with $379,684. Your profit was $259,684. That is more than 2x your investment.

Inflation – Why Your Real Returns Matter

Here is something most calculators do not show. Inflation eats away your purchasing power.

Nominal Returns vs Real Returns

Nominal return: The actual percentage your money grew. Real return: Your growth minus inflation.

Example:

- Your investment grew 10% last year

- Inflation was 3%

- Your real return was only 7%

Why This Matters for Retirement Planning

Scenario: You plan to retire in 30 years with $1,000,000.

- At 3% inflation, that $1,000,000 will only buy what $412,000 buys today.

- To have the same purchasing power as $1,000,000 today, you actually need about $2,427,000 in 30 years.

What I do now: I always calculate my retirement goal in today's dollars. Then I add inflation to see what I really need.

Taxes – How They Reduce Your Investment Growth

I ignored taxes for years. That was a mistake.

Example: $10,000 invested for 20 years at 10% returns

Without taxes:

- Final amount = $67,275

- Profit = $57,275

With 15% capital gains tax on profit:

- Tax on profit = $57,275 × 0.15 = $8,591

- After-tax amount = $67,275 - $8,591 = $58,684

What happened: You lost $8,591 to taxes. That is money that could have stayed invested and grown.

My advice:

- Use tax-advantaged accounts when possible (401k, IRA, Roth)

- Hold investments for more than 1 year for lower long-term capital gains rates

- Calculate after-tax returns for realistic planning

Goal Planning – How Much to Invest Monthly to Reach Your Target

This is the most practical use of an investment calculator. You have a goal. You want to know how much to save each month.

Example 1: Retirement Goal

Your goal: $1,000,000 in 25 years Expected return: 8% per year Current savings: $0

Calculation:

- Monthly investment needed = about $1,050

What this means: If you invest $1,050 every month for 25 years at 8% returns, you will have about $1,000,000.

Example 2: Child Education Goal

Your goal: $200,000 in 15 years for college Expected return: 7% per year Current savings: $10,000 already saved

Calculation:

- Monthly investment needed = about $600

What this means: With $10,000 already saved, you need to add $600 per month for 15 years to reach $200,000.

Example 3: Home Down Payment

Your goal: $100,000 in 5 years Expected return: 5% per year (conservative for short term) Current savings: $20,000

Calculation:

- Monthly investment needed = about $1,150

What this means: You need to save $1,150 per month for 5 years to reach your $100,000 down payment goal.

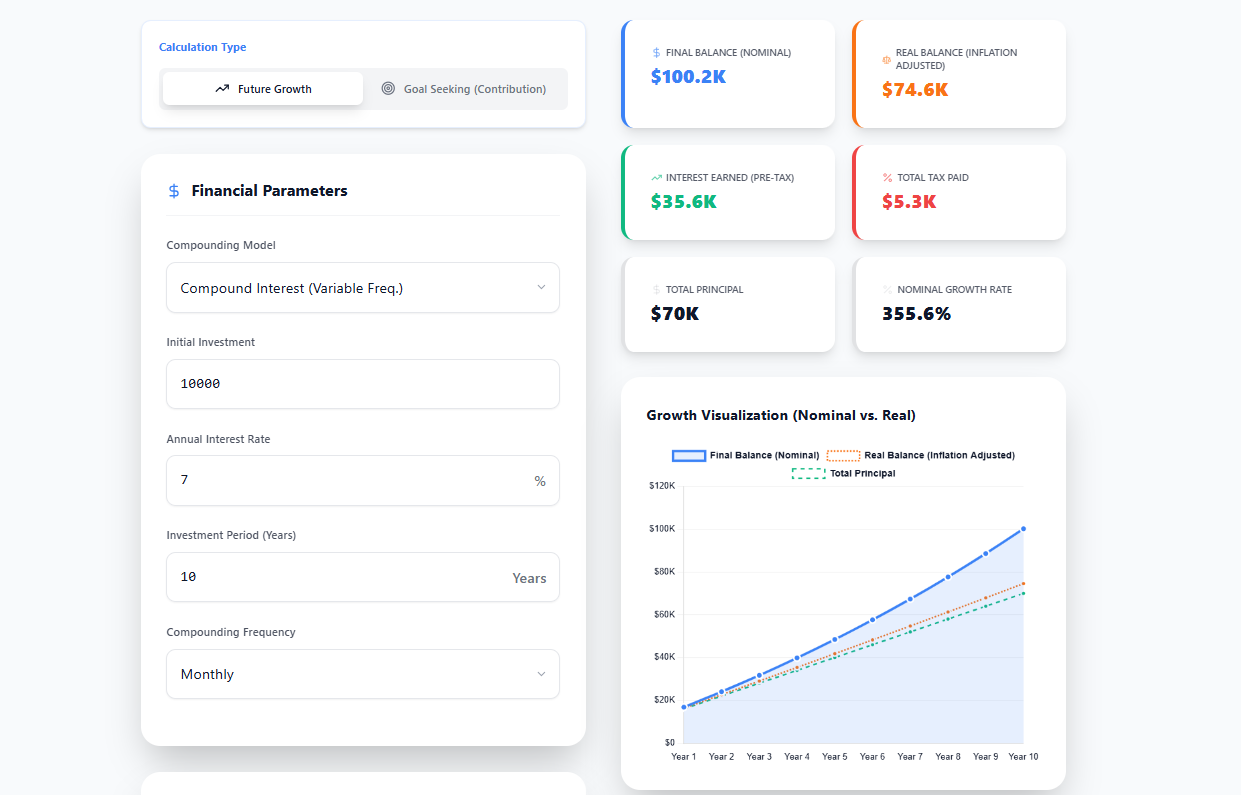

How to Use Our Investment Growth Calculator

Our investment growth calculator handles all these scenarios.

Step 1: Choose what you want to calculate

- Growth Mode: See how your investments grow over time

- Goal Mode: Find out how much to invest monthly to reach a target

Step 2: Enter your basic information

- Initial investment (lump sum)

- Expected annual return rate

- Number of years

- Compounding frequency (monthly, quarterly, annually, etc.)

Step 3: Add regular contributions (optional but important)

- How much you add each month or year

- When you add it (start of period or end)

Step 4: Add economic adjustments (for realistic planning)

- Tax rate on investment gains

- Expected inflation rate

Step 5: See your results

- Final balance (nominal)

- Real balance (inflation-adjusted)

- Total interest earned

- Total taxes paid

- Year-by-year growth schedule

- Interactive growth chart

All calculations happen in your browser. Your data never leaves your device.

Real Investment Growth Examples from Different Scenarios

Example 1: Young Professional Starting Late

Profile: Sarah, age 40, wants to retire at 65 Current savings: $50,000 Monthly contribution: $1,000 Expected return: 8% Inflation: 3% Tax rate: 15%

Results:

- After 25 years (age 65):

- Nominal balance: About $1,080,000

- Real balance (inflation-adjusted): About $540,000

- Total taxes paid: About $60,000

Sarah's take: She wishes she started earlier. With 10 more years, her real balance would be nearly double.

Example 2: Early Starter

Profile: Mike, age 25, wants to retire at 60 Current savings: $10,000 Monthly contribution: $500 Expected return: 8% Inflation: 3% Tax rate: 15%

Results:

- After 35 years (age 60):

- Nominal balance: About $1,340,000

- Real balance (inflation-adjusted): About $580,000

- Total invested: $10,000 + ($500 × 420 months) = $220,000

Mike's take: He invested only $220,000 but ended with $1.34 million. The power of time and compounding.

Example 3: High Earner, Late Start

Profile: David, age 45, wants to retire at 60 Current savings: $100,000 Monthly contribution: $3,000 Expected return: 7% (more conservative due to shorter timeline) Inflation: 3% Tax rate: 20%

Results:

- After 15 years (age 60):

- Nominal balance: About $1,020,000

- Real balance (inflation-adjusted): About $650,000

- Total invested: $100,000 + ($3,000 × 180 months) = $640,000

David's take: He has to save aggressively because he started late. But it is still possible to retire comfortably.

Example 4: Goal Planning for Home Purchase

Profile: Priya and Raj, want $150,000 for home down payment in 4 years Current savings: $30,000 Expected return: 6% (conservative for short term) Inflation: Not relevant for short term Tax rate: 10% on gains

Using goal mode:

- Required monthly contribution = About $2,200

Their plan: Save $2,200 per month for 4 years. Combined with their $30,000 savings, they will reach $150,000.

Common Investment Growth Mistakes I Have Made

Mistake 1: Underestimating the Power of Time

What I did wrong: I started investing seriously at age 35 instead of 25.

The cost: Every $10,000 invested at 25 would have grown to about $45,000 by age 45. The same $10,000 invested at 35 grew to only about $22,000 by age 45.

What I learned: Start as early as possible. Even small amounts matter.

Mistake 2: Ignoring Fees

What I did wrong: I paid 1.5% in annual fees on a mutual fund without realizing it.

The cost: On a $100,000 portfolio over 20 years, 1.5% fees cost me about $50,000 in lost growth.

What I learned: Compare expense ratios. Lower fees = more money in your pocket.

Mistake 3: Expecting Unrealistic Returns

What I did wrong: I assumed 15% returns every year.

The cost: When the market returned only 8%, I felt like I was failing. I made emotional decisions and sold at bad times.

What I learned: Use realistic return assumptions (8-10% for stocks, 4-6% for bonds).

Mistake 4: Not Adjusting for Inflation

What I did wrong: I thought $1 million at retirement would be plenty.

The cost: With 3% inflation over 30 years, $1 million is worth only $412,000 in today's dollars.

What I learned: Always calculate real returns, not just nominal returns.

Mistake 5: Stopping Contributions During Market Drops

What I did wrong: In 2008, I stopped my monthly contributions because the market was crashing.

The cost: I missed buying stocks at low prices. When the market recovered, I had fewer shares.

What I learned: Keep investing regularly. Market downturns are the best time to buy.

Frequently Asked Questions

Q: How to calculate compound interest on an investment?

A: Use the formula: Future Value = Principal × (1 + Rate ÷ Frequency) ^ (Frequency × Years). Or use our investment calculator for instant results.

Q: What is the difference between compound interest and simple interest?

A: Simple interest earns returns only on your original investment. Compound interest earns returns on your original investment AND on previous returns. Compound interest grows much faster over time.

Q: How to calculate future value of monthly investments?

A: Use an investment calculator with regular contributions. Enter your monthly amount, expected return, and number of years. The calculator shows the future value.

Q: How much will my investment grow in 10 years?

A: Depends on your return rate. At 8% annual return, $10,000 grows to about $21,589 in 10 years. Use our calculator with your specific numbers.

Q: What is a good rate of return for investments?

A: Stock market averages about 10% per year over long periods. Bonds average 4-6%. Real estate averages 8-12%. Higher returns usually come with higher risk.

Q: How to calculate investment growth with inflation?

A: Calculate your nominal growth first. Then divide by (1 + inflation rate) ^ years. Our calculator does this automatically.

Q: How much to invest monthly to reach $1 million?

A: Depends on your timeline and expected returns. At 8% returns, you need about $1,050 per month for 25 years. Our goal mode calculator tells you exactly.

Q: What is the rule of 72?

A: A quick way to estimate how long it takes to double your money. Divide 72 by your annual return rate. At 9% returns, 72 ÷ 9 = 8 years to double.

Q: How does compounding frequency affect returns?

A: More frequent compounding gives slightly higher returns. Daily compounding is better than annual compounding, but the difference is small over short periods.

Q: Should I include taxes in my investment calculation?

A: Yes. Taxes reduce your actual returns. Always calculate after-tax returns for realistic planning.

Q: What is the best investment calculator online?

A: Our investment growth calculator is free, handles regular contributions, inflation, taxes, and goal planning. It shows year-by-year growth and charts.

Q: How to calculate retirement corpus needed?

A: Estimate your annual retirement expenses. Multiply by 25 (for 4% withdrawal rule). For $50,000 annual expenses, you need $1,250,000. Our calculator helps you plan how to reach that goal.

Q: What is the difference between nominal and real returns?

A: Nominal returns are the actual percentage your money grew. Real returns are nominal returns minus inflation. Real returns matter more because they show your actual purchasing power.

Q: How to calculate investment growth for SIP?

A: For regular monthly investments, use the future value of annuity formula. Our calculator handles this automatically. Enter your monthly amount, expected return, and years.

Q: Is the investment calculator free?

A: Yes. Completely free. No signup. No limits. Use it as much as you want.

My Final Advice (From 15+ Years of Investing)

After investing for over 15 years, here is what I have learned about investment growth.

Start today, not tomorrow. The single biggest factor in investment growth is time. Every year you delay costs you years of compounding.

Use realistic return assumptions. Do not plan for 15% returns. Use 8-10% for stocks. If you get more, great. If you get less, you are still prepared.

Include inflation and taxes. Your nominal returns do not matter as much as your real after-tax returns. Calculate both.

Make regular contributions automatic. Set up auto-investing from your paycheck or bank account. You will not miss the money, and your investments will grow consistently.

Do not stop during market downturns. This is when investments are on sale. Keep investing. Your future self will thank you.

Use a calculator before every major investment decision. I learned this after making expensive mistakes. Run the numbers first. If the math does not make sense, do not invest.

Review your plan annually. Life changes. Goals change. Markets change. Review your investment plan once a year and adjust as needed.

Be patient. Investment growth is slow at first. After 5-10 years, you will start to see the power of compounding. After 20-30 years, it becomes remarkable.

And finally, use a good investment calculator. Our tool handles compound interest, regular contributions, inflation, taxes, and goal planning. It is free and works anywhere.

Calculate Your Investment Growth Now – Free Tool

Have questions about calculating investment growth for your specific situation? Leave a comment below. I try to answer every one.

Tags: investment growth calculator, how to calculate compound interest, compound interest formula explained, future value calculator, investment return calculator, sip investment calculator, monthly investment calculator, retirement corpus calculator, goal planning calculator, inflation adjusted returns, real returns vs nominal returns, compound interest vs simple interest, daily compound interest calculator, monthly compound interest formula, annual compound interest calculator, investment growth over time, how to calculate future value of investment, investment calculator with regular contributions, investment calculator with inflation, investment calculator with tax, compound interest for beginners, investment growth chart, year by year investment growth, how much will my investment grow, lump sum investment calculator, recurring investment calculator, power of compounding explained, time value of money calculator, financial goal planning, target corpus calculator, required monthly investment for goal, investment growth rate calculator, cagr calculator for investments, investment planning for retirement, investment planning for child education, investment planning for home purchase, best investment calculator online free, investment growth projection tool